In this post we will cover option valuation using only simple math that a sixth grader could do (_my sixth grader did it_) and lay the groundwork for thinking in [[Thinking Probabilistically|terms of probability]]. We will not use the famous Black Scholes model or any advanced calculus that most modern day option valuation models use. We will not talk about the Greeks. Options are choices and everyone faces choices in daily life. Thinking about these choices in a probabilistic manner can help us improve our decision making process.

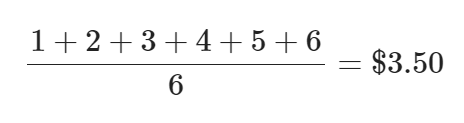

To start, let’s consider a simple roll of a die: What is the fair value of a bet where you are paid the amount you roll? To answer this we need to compute the expected value of the bet:

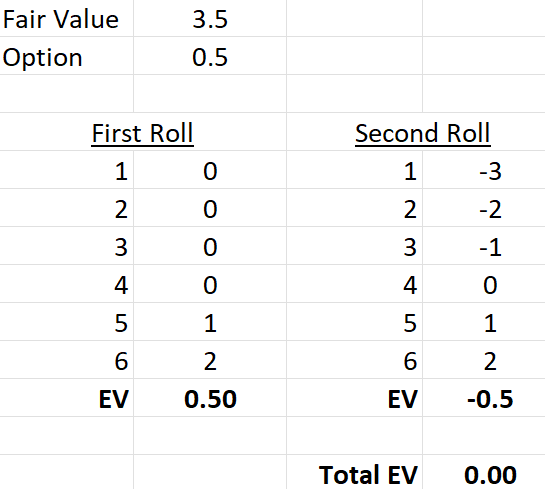

The average of the possible outcomes when rolling a single die is $3.50. If you pay $3.00 for this bet you can expect to earn a profit of $0.50 for each bet over the long-run, if you pay $4.00 you can expect to lose $0.50 for each bet over the long run. Notice that you may pay $4 and roll a six and earn a $2 profit, just like you may pay $3 and roll a one, losing $2; but over multiple rolls you can expect that the average of your accumulated profits and losses will converge to your expected value as seen below.

Now, lets change the bet to pay only if you roll a number greater than 3. What is the fair value of this bet?

We have just priced an option! What makes this an option is that we are only considering a subset of the potential outcomes. When we face choices in life we are usually looking at the alternatives and considering the potential outcomes from a given choice of action. If we take the highway on our commute home we have a faster and more direct route home but we might hit traffic. This framework for thinking about choices as options and evaluating them probabilistically can help us in everyday life.

But we aren’t all the way there yet. We could consider this to be the 4 strike call option[^1] but it is not really the same thing. A call option gives you the right, but not the obligation, to buy the underlying at the strike price over a set period of time. So there are actually two choices we make: first to buy the call option and second, to exercise the option. To understand this in terms of our simple roll of the die, we need to consider what we would pay for the option to re-roll(_i.e. exercise the option_).

If we paid $3.50 for the roll of the die[^2], what is the fair value of the option to roll a second time? We would only want to re-roll if we rolled a 1,2, or 3 since we paid $3.50 for the bet. There is a 50% chance we roll a 1,2, or 3 and take the option to roll again. On the second roll we again have a 50% chance of rolling a 4,5, or 6. But we also need to factor in the cost of the option in our potential payoff scenarios, therefore it is easier to just map out the different potential outcomes and figure out what option price would make you breakeven over all the outcomes (_i.e. the option’s fair value_). In this case the option to re-roll is worth $0.50:

Notice that on the first roll you exercise the option to roll a second time if you roll any number between 1 and 4 for the chance on the second roll to roll a 5 or 6 since your all-in-cost of bet plus the option premium is $4.00.

The value of the option to re-roll is dependent on the price you pay to roll the die once and you obviously must choose to buy the option prior to your first roll. This introduces some interesting nuances which depend on your attitude towards risk. If you can buy the bet for $1 you have no downside risk and many people would not choose to pay more for the option to re-roll, especially since it rises in price to account for the lower strike price. However, the option to re-roll gives you more chances to win more so statistically speaking it make sense to buy the option even though it increases your chances of taking a loss.

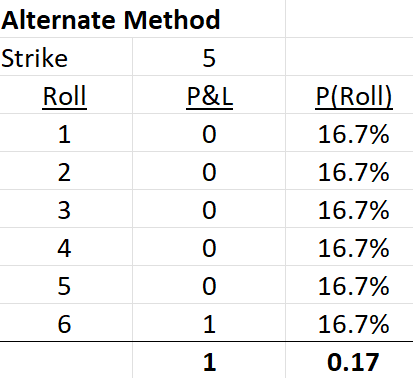

While we used the example of the option to re-roll to introduce a way to value an option, a call option has a fixed strike that is independent of the price of the underlying. Therefore we can use another, easier way to arrive at its value which is to compute the payoff of the call for each potential outcome and divide it by the total number of outcomes for a single roll of the die.

We did this for the 5-strike call so that we can compare it to another option pricing method we will cover in the next section. Do this for the 4 strike call on your own to confirm the value we came up with in the prior example.

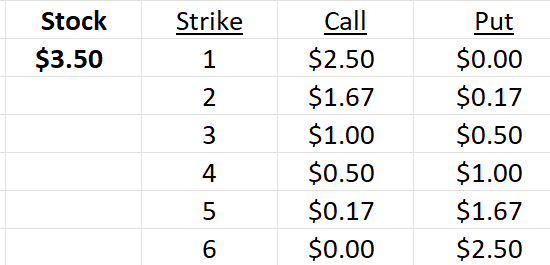

Now that we have the idea of the fair value of a bet (_stock price_) and the strike price, 4 in our example, we can use this methodology to price equity call and put options that we see in the market.

# **Put-Call Parity**

Put-Call parity is an important equality that helps you understand the arbitrage relationship between calls and puts of the same strike. It tells us that if you own a call and are short a put with the same strike you have the same position as owning the stock. This is because no matter where the stock is at expiration you will either exercise the call or be assigned on the short put. This equation allows us to think of options and the underlying stock as interchangeable parts. The equation is:

The reversal/conversion accounts for the carry cost of the stock (_how much it would cost to borrow money to buy the stock plus the dividends you would receive_). This is important because if you buy a call you do not need to pay the full price of the stock and therefore save the opportunity cost of keeping the money in cash earning the short-term rate but you do not receive the dividends the stock may pay before expiration. Similar logic applies to puts.

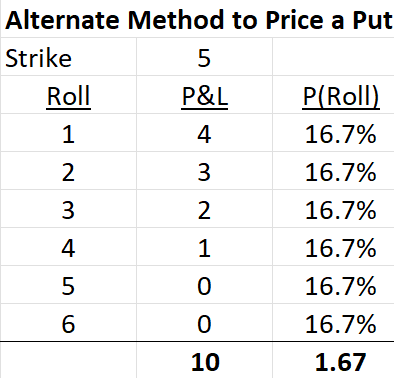

For our purposes we will ignore the reversal/conversion and just use a reduced put-call parity to price options on our dice roll game. We could start by pricing the calls using either method we developed earlier but in this case we want to confirm those values by pricing the puts first and then using put-call parity to confirm the prices we got earlier. So let’s start with the 5-strike puts:

First we need to re-arrange the put-call parity equation to derive the value of the 5-strike call:

Now we have confirmed, by put-call parity, that the value of the 5-strike call we derived earlier is correct. Now we can repeat this process for all the other strikes to get a full option chain for our die roll game.

# **Spreads**

Now that we have priced a full option chain on our game we will quickly define different option spreads. Spreads give us a way to bet on discrete outcomes within the distribution of overall outcomes. When I started in the business options traders would compute the implied probability distribution from options prices using spread pricing. Today, anyone can get this analysis from brokers like Interactive Brokers using their option valuation software. This is helpful to understand if the market is betting on different outcomes being more likely than others.

This is not an exhaustive list, but simply some of the most popular spread strategies used to bet on different outcomes:

**Bull Spreads(aka Vertical Spreads)**

- short a higher strike put and long a lower strike put

- long a lower strike call and short a higher strike call

**Bear Spreads(aka Vertical Spreads)**

- short a lower strike call and long a higher strike call

- long a higher strike put and short a lower strike put

**Butterfly Spreads**

- long a lower strike call, long a higher strike call, short 2 middle strike calls

- long a higher strike put, long a lower strike put, short 2 middle strike puts

**Calendar Spreads**

- long a near dated option and short an out month option

- short a near dated option and long an out month option

# **How to read probabilities from option prices**

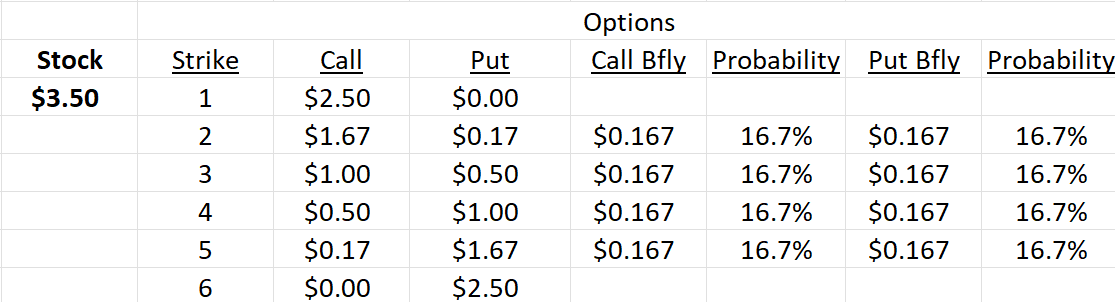

If we compute the prices of all the butterfly spreads we can infer the probability that the market assigns to each outcome. Butterfly spreads are a way to bet on the stock closing within a narrowly defined range at expiration. In our game, we can use it to calculate what the option prices imply for the odds of each possible roll of the die.

A call butterfly is when you buy one lower strike call, one higher strike call, and sell two middle strike calls. For example, the 2 strike call fly is calculated by taking the price of the 1 strike and the 3 strike and subtracting the price of two of the 2 strike calls:

The price of the 2 strike call fly is $0.167. To get the probability from that price we just divide by the strike difference of the fly which is 1 in this case (_1–2–3 fly_).

Therefore, we can see that our option prices have correctly told us that the odds of rolling a 2 (the 2 strike fly) is 16.7% or 1/6.

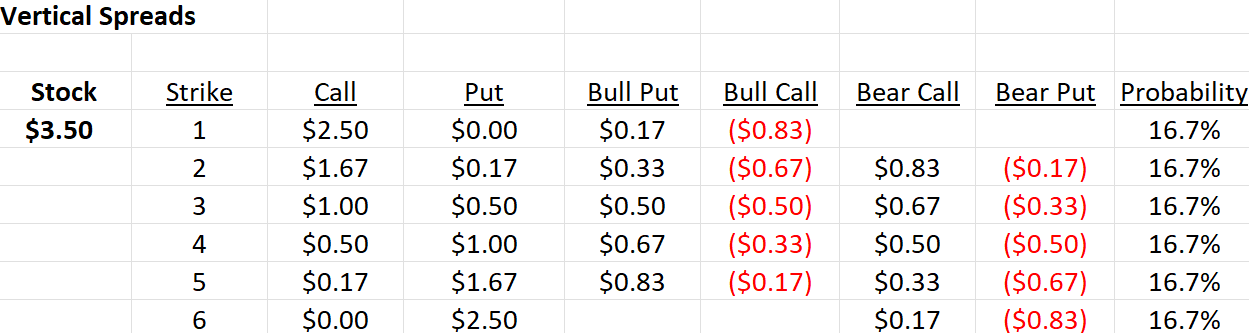

Since we don’t have a 0-strike or a 7-strike we were not able to price the butterflies at the top and bottom of our option chain. Instead, we can use call or put spreads to determine the probability the market is assigning to the 1-strike and the 7-strike outcomes.

A Bull Put spread entails you selling a higher strike put and buying a lower strike put. The higher strike put has a higher premium that you hope to pocket and buying the lower strike put limits your downside risk. Therefore, the difference in the premiums divided by the strike difference is the probability the market assigns to the outcome being between the two strikes at expiration.

In our example if we sell the 2-strike put at $0.167 and buy the 1-strike put for $0 we pocket $0.167 for a any roll of 2 or higher. If a 1 is rolled we get assigned on the 2-strike put we sold and pay the option holder $1.00. Therefore, the market assigned probability is 16.7% or 1/6 for rolling a 1. Said differently, if you wanted to bet on rolling a 1, you would buy the 1/2 put spread from me for $0.167 or 16.7% of your potential payout.

For Bull Put or Bear Call spreads we are selling higher priced options and buying lower priced options so we are taking in premium and hoping that any other outcome above (in the case of the bull put) or below (in the case of the bear call) the strike we sold happens. By taking in premium our upside is limited to the premium and the downside is limited to the difference in the strikes. For Bear Put or Bull Call spreads we are betting on the opposite thing: we are buying the more expensive option and offsetting the cost of that by selling a lower priced option. Therefore we want the outcome to be below (for the bear put) or above (for the bull call) the strike we bought. We are paying premium for this bet so our downside is limited to the premium and our upside is limited to the difference in the strikes. At this point you should start to see that a combination of call and put spreads will basically give you a butterfly spread since the upside and downside offset leaving you betting on a single outcome. For example, if you combine the 2/3 bear call spread with the 1/2 bull put spread, you have sold the 2-strike twice and bought the 1 and 3 strikes. This is slightly different than the traditional butterfly spread we described above but gives you the same payout profile. You could also combine the 1/2 and 2/3 call spreads to give you a traditional 1/2/3 call butterfly.

# Wrapping Up

We have developed a simple framework to value bets and options by thinking in terms of probability. We priced options using two different methods: 1) re-roll of a die and 2) put-call parity to show what options are and how they work. We also used this framework to understand how we can bet on discrete outcomes within the distribution of possible outcomes for our game. This framework is the foundation for a deeper exploration into options theory and provides a simple architecture for thinking about different payout structures in the market.

Most practitioners use options to observe market expectations for different outcomes just like we were able to read probabilities of certain prices from butterfly and vertical spreads. In fact, some believe that options are the actual underlying because they provide a direct path to betting on finite market outcomes. In this view, the underlying is actually just a bunch of options rolled up into a single price.

Whatever way you choose to think about these things the important takeaway from this article should be a framework for [[Thinking in Bets]] and an understanding that the financial markets are just a collection of bets. The most profitable investors and traders can realize this and look for mispriced bets or ones that offer favorable payoff profiles. Thinking in this manner helps you to separate your biases about what you want the market to do from the real and measurable odds that the market is giving you for your bet. No matter how strongly you feel about something, if you are not getting paid to take that risk then you shouldn’t take the risk.

**Case Studies:**

- [CHG Issue #40: Options](https://cedarshillgroup.substack.com/p/chg-issue-40-options)

Explore Further:

- [[Getting the Best of It]] by David Sklansky

- Options, Futures, & Other Derivatives by John C. Hull

- www.raiseyourgame.com

- www.moontowermeta.com

- [[Ergodicity]]

Tags: #seeds

Your support for Cedars Hill Group is greatly appreciated

<form action="https://www.paypal.com/donate" method="post" target="_top">

<input type="hidden" name="hosted_button_id" value="74PGN8ZXHQVHS" />

<input type="image" src="https://www.paypalobjects.com/en_US/i/btn/btn_donate_LG.gif" border="0" name="submit" title="PayPal - The safer, easier way to pay online!" alt="Donate with PayPal button" />

<img alt="" border="0" src="https://www.paypal.com/en_US/i/scr/pixel.gif" width="1" height="1" />

</form>

[^1]: We consider it the 4 strike because the option is for any number **greater than** 3. Call strikes are generally expressed as **greater than or equal to** and put strikes are **less than or equal to.** Since we only care about rolls greater than three that is also considered **greater than or equal to 4.**

[^2]: $3.50 is considered the fair value of the bet in this case